Introduction: Why Vehicle Insurance Pricing Is More Psychological Than Mathematical

Vehicle insurance pricing is widely assumed to be driven purely by mathematics, algorithms, and actuarial science. While these technical components are essential, they tell only part of the story.

In reality, insurance pricing is deeply shaped by how people think, feel, and behave when confronted with risk and uncertainty. Insurance companies do not simply calculate probabilities; they design pricing systems that align with human psychology, anticipating emotional reactions such as fear, anxiety, trust, and perceived fairness. This psychological layer helps explain why insurance pricing often feels confusing, inconsistent, or even unfair to consumers.

Table of Contents

At its core, vehicle insurance operates in a space where logic and emotion collide. Drivers are asked to pay for protection against events they hope will never occur, which creates mental resistance. Insurers respond by structuring premiums and coverage options in ways that feel emotionally acceptable rather than strictly rational. These strategies are built around predictable human tendencies, including:

- Fear of financial loss

- Overconfidence in personal driving ability

- Desire for control over outcomes

- Sensitivity to price comparisons

- Need for trust and reassurance

Understanding these psychological drivers allows readers to see insurance pricing not as a random or manipulative system, but as one designed to function within real human behavior.

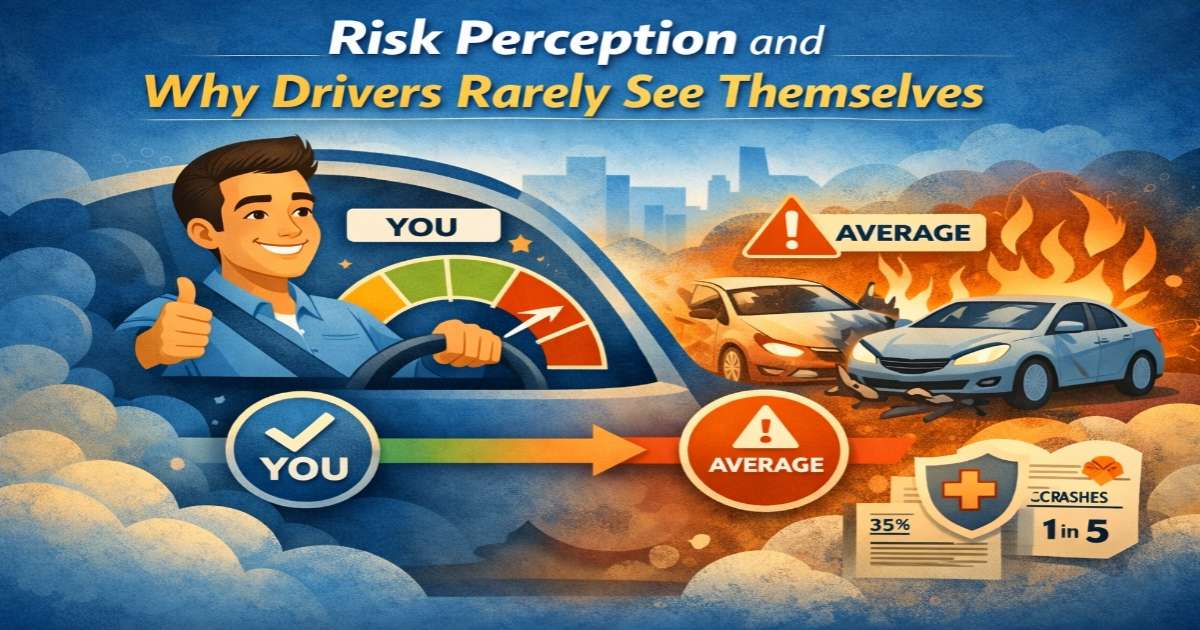

Risk Perception and Why Drivers Rarely See Themselves as High Risk

One of the most influential psychological factors behind vehicle insurance pricing is risk perception. Most drivers genuinely believe they are safer than the average person on the road. This optimism bias leads individuals to underestimate their likelihood of accidents, claims, or costly incidents. Insurance companies, however, must rely on statistical realities rather than personal beliefs, creating a disconnect that often frustrates consumers.

Insurers account for this gap by breaking risk into indirect, less personal factors rather than confronting drivers with blunt assessments. Common pricing elements include:

- Driving history and prior claims

- Geographic location and traffic density

- Vehicle type, repair costs, and safety ratings

- Age group and driving experience

- Annual mileage and usage patterns

Psychologically, these factors feel external and impersonal, making higher premiums easier to accept. Instead of telling a driver they are “high risk,” insurers attribute pricing to data points that appear neutral. This approach reduces emotional resistance while still allowing insurers to price risk accurately across large populations.

Loss Aversion: Why Fear Matters More Than Logic

Loss aversion plays a central role in vehicle insurance pricing because people fear losses more intensely than they value equivalent gains. The possibility of facing a large financial burden after an accident feels far more painful than the ongoing cost of paying insurance premiums. Insurers leverage this instinct by framing premiums as a form of protection rather than an expense.

This psychological tendency explains why many drivers choose higher coverage limits or lower deductibles even when the math suggests otherwise. Key pricing elements influenced by loss aversion include:

- Higher premiums for lower deductibles

- Optional add-ons such as roadside assistance

- Comprehensive and collision coverage upgrades

- Accident forgiveness programs

By positioning insurance as a safeguard against worst-case scenarios, insurers align pricing with emotional decision-making. The fear of sudden loss outweighs rational cost comparisons, making consumers more willing to accept higher premiums for peace of mind.

Trust, Brand Reputation, and Emotional Security

Vehicle insurance is fundamentally a promise, not a physical product. Because its value is realized only during stressful situations, trust becomes a powerful pricing factor. Consumers are often willing to pay more to insurers they believe will treat them fairly during claims. This emotional security allows established brands to maintain higher premiums without losing customer loyalty.

From a psychological perspective, trust is reinforced through:

- Brand recognition and long market presence

- Clear policy language and transparency

- Consistent customer service messaging

- Fast and fair claims reputation

When consumers trust an insurer, they perceive less risk in paying higher premiums. Pricing, in this sense, reflects emotional confidence as much as actuarial probability.

Social Comparison and the Need to Feel “Normal”

People rarely evaluate insurance costs in isolation. Instead, they compare their premiums to what others claim to pay. This social comparison strongly influences satisfaction, even when coverage levels differ. Insurers anticipate this behavior and design pricing that feels socially reasonable.

Common comparison triggers include:

- Friends or family sharing premium amounts

- Online quote comparison tools

- “Average cost” marketing messages

- Regional or demographic benchmarks

If a premium feels aligned with perceived norms, it is more likely to be accepted. If it feels unusually high, dissatisfaction increases regardless of actual value. Insurers use this insight to frame pricing competitively rather than purely numerically.

Behavioral Incentives and the Illusion of Control

Drivers strongly prefer to believe they have control over their insurance costs. Insurers reinforce this belief through behavior-based pricing models that reward certain actions. These incentives increase engagement and reduce resentment toward premiums.

Common behavior-based pricing strategies include:

- Safe-driver discounts

- Usage-based or telematics programs

- Claim-free bonuses

- Bundling incentives

Even when these programs do not dramatically reduce overall costs, they improve customer satisfaction by creating a sense of fairness and agency. Psychologically, feeling in control is often more valuable than actual savings.

Final Verdict: Pricing Insurance for Humans, Not Just Data

Vehicle insurance pricing is not solely about predicting accidents—it is about predicting behavior. Insurers design pricing systems that reflect how people perceive risk, respond to fear, seek reassurance, and compare themselves to others. Understanding these psychological foundations helps explain why premiums are structured the way they are and why they often feel emotional rather than logical.

For consumers, this awareness turns frustration into insight. Insurance pricing becomes easier to navigate when it is seen as a human system shaped by emotion, perception, and behavior—not just numbers on a spreadsheet.

Frequently Asked Questions (FAQS)

Q.1: What is the psychology behind vehicle insurance pricing?

The psychology behind vehicle insurance pricing refers to how insurers use human behavior, emotions, and decision-making patterns to determine car insurance premiums. Instead of relying only on accident statistics, insurers consider how drivers perceive risk, fear financial loss, compare prices, and respond to uncertainty. These psychological factors influence how pricing is structured, explained, and accepted by consumers, making insurance premiums as much a behavioral product as a mathematical one.

Q.2: How does psychology affect car insurance premiums?

Psychology affects car insurance premiums by shaping how drivers react to risk and uncertainty. Factors such as loss aversion, optimism bias, and perceived control influence pricing decisions. Insurers design premiums, deductibles, and coverage options based on how likely drivers are to accept prices, avoid policy changes, or file claims. This behavioral approach allows insurers to balance profitability with customer satisfaction.

Q.3: Why does vehicle insurance pricing vary so much between drivers?

Vehicle insurance pricing varies because insurers evaluate both statistical risk and behavioral indicators. Even small differences in location, driving frequency, or demographic patterns can affect how insurers predict future claims. Additionally, pricing reflects how different drivers respond psychologically to risk and coverage options, which is why two similar drivers may still receive different premiums.

Q.4: Why do safe drivers still pay high car insurance premiums?

Safe drivers often pay high car insurance premiums because pricing is based on population-level risk rather than individual confidence. Many drivers overestimate their own safety due to optimism bias, while insurers rely on historical data and behavioral trends. Insurance pricing also accounts for claim likelihood, not just accident probability, which can keep premiums high even for cautious drivers.

Q.5: How do insurance companies calculate vehicle insurance pricing?

Insurance companies calculate vehicle insurance pricing using a combination of actuarial data and behavioral psychology. While statistical models estimate accident risk, psychological insights help determine pricing structures that drivers will accept. Insurers consider factors such as risk perception, loss avoidance, trust in the brand, and consumer response to deductibles and discounts.