Hidden Costs of Vehicle Loans In 2026

Buying a car is often an emotional decision. The excitement of owning a new or used vehicle can easily overshadow the fine print of a vehicle loan agreement. While lenders usually highlight attractive interest rates and affordable monthly payments, there are many hidden costs of vehicle loans that borrowers only discover much later.

Table of Contents

These overlooked expenses can quietly increase the total cost of your car by thousands, turning what seemed like a smart financial move into a long-term burden.

The Illusion of Low Monthly Payments

Many lenders structure vehicle loans to focus your attention on a low monthly payment rather than the overall cost of the loan. This approach makes the loan appear affordable, but it often hides the reality of how much you are truly paying over time. By extending the loan term from four years to six or even seven years, lenders reduce monthly payments while significantly increasing the total interest paid.

Key points often hidden behind low monthly payments include:

- Longer loan terms mean you pay interest for more years

- The total repayment amount can be far higher than the car’s actual value

- You may still owe money even after the vehicle’s resale value drops sharply

This strategy benefits lenders more than borrowers, especially when buyers focus only on short-term affordability rather than long-term cost.

Interest Rates That Aren’t as Simple as They Seem

Interest rates advertised by lenders are often “best-case” scenarios. These rates typically apply only to borrowers with excellent credit scores, stable income, and strong financial histories. If your credit profile doesn’t meet these standards, you may be approved at a much higher rate without fully realizing the impact.

Hidden interest-related costs may include:

- Variable interest rates that increase over time

- Higher rates applied after initial promotional periods

- Additional interest charged due to payment scheduling methods

Even a small increase in interest rate can result in paying hundreds or thousands more over the life of the loan, making it crucial to understand exactly how your interest is calculated.

Fees That Quietly Inflate Your Loan

Vehicle loans often come with a variety of fees that are rarely discussed upfront. These charges may seem minor individually, but together they can significantly increase your borrowing cost. Many borrowers only notice these fees after reviewing detailed loan statements or closing documents.

Common hidden fees include:

- Loan origination or processing fees

- Documentation and administrative charges

- Early repayment or prepayment penalties

- Late payment and rescheduling fees

Because these fees are usually bundled into the loan, borrowers end up paying interest on them as well, further increasing the total cost.

Add-Ons That Sound Helpful but Cost More

Lenders and dealerships often bundle optional products into vehicle loans, presenting them as essential protections. While some add-ons can be useful, many are overpriced or unnecessary, especially when financed over several years.

Frequently overlooked add-ons include:

- Extended warranties with limited coverage

- Gap insurance priced higher than market rates

- Credit life or disability insurance

- Paint protection or service packages

When these extras are financed, you don’t just pay their base price—you also pay interest on them, which can dramatically inflate their true cost.

Depreciation and Negative Equity Traps

Vehicles depreciate faster than most other purchases, yet lenders rarely emphasize how this affects your loan. In many cases, borrowers owe more on their loan than the car is worth, especially in the early years. This situation, known as negative equity, can trap you financially.

Hidden risks of depreciation include:

- Difficulty selling or trading in the vehicle

- Rolling old debt into a new loan

- Higher financial loss in case of theft or total damage

Without proper planning, depreciation can lock you into a loan longer than you intended.

Insurance Costs That Rise with Financing

Financing a vehicle often comes with stricter insurance requirements. Lenders usually require comprehensive and collision coverage to protect their investment, which can significantly increase your insurance premiums.

Additional insurance-related costs may involve:

- Mandatory higher coverage limits

- Increased premiums for newer vehicles

- Required gap coverage in some loan agreements

These ongoing costs are rarely factored into the initial affordability discussion but can strain your monthly budget over times.

Refinancing Isn’t Always the Money-Saver It Appears to Be

Many borrowers believe refinancing a vehicle loan will automatically reduce their financial burden, but this is another area where hidden costs can quietly appear. While refinancing may lower your monthly payment, it often extends the loan term, meaning you continue paying interest for a longer period. Some lenders also charge refinancing fees that cancel out the savings you expect to gain.

Important refinancing costs and risks include:

- New loan origination or processing fees

- Resetting the loan term, which increases total interest paid

- Higher interest rates if your credit score has changed

- Loss of benefits from your original loan agreement

Before refinancing, it’s essential to calculate the total repayment amount rather than focusing solely on monthly relief.

Early Payoff Isn’t Always Rewarded

It seems logical that paying off your vehicle loan early would save money, but that’s not always the case. Some lenders include early payoff or prepayment penalties that punish borrowers for settling their debt ahead of schedule. These penalties are rarely discussed upfront and are buried deep in loan agreements.

Hidden early payoff issues may involve:

- Flat-rate prepayment penalties

- Interest front-loading that limits savings

- Administrative charges for closing the loan early

Understanding whether your loan penalizes early repayment can help you avoid unexpected costs when your financial situation improves.

Credit Score Impact You Might Not Expect

Vehicle loans affect your credit profile in ways that lenders don’t always explain clearly. While making on-time payments can improve your credit, missed or late payments—even by a few days—can cause noticeable damage. Additionally, applying for multiple loans in a short period can temporarily lower your score.

Credit-related hidden costs include:

- Higher interest rates due to small credit score drops

- Reduced approval chances for future loans

- Increased insurance premiums tied to credit history

These indirect costs can extend far beyond the life of the vehicle loan itself.

Dealer Financing vs. Bank Loans: The Cost Difference

Dealer financing is often marketed as convenient and fast, but that convenience can come at a price. Dealerships sometimes mark up interest rates offered by banks or finance companies, earning a commission without clearly disclosing it to the buyer.

Potential hidden costs of dealer financing include:

- Marked-up interest rates above lender offers

- Bundled add-ons that are hard to decline

- Less transparent loan terms

Comparing dealer offers with bank or credit union pre-approvals can reveal significant savings opportunities.

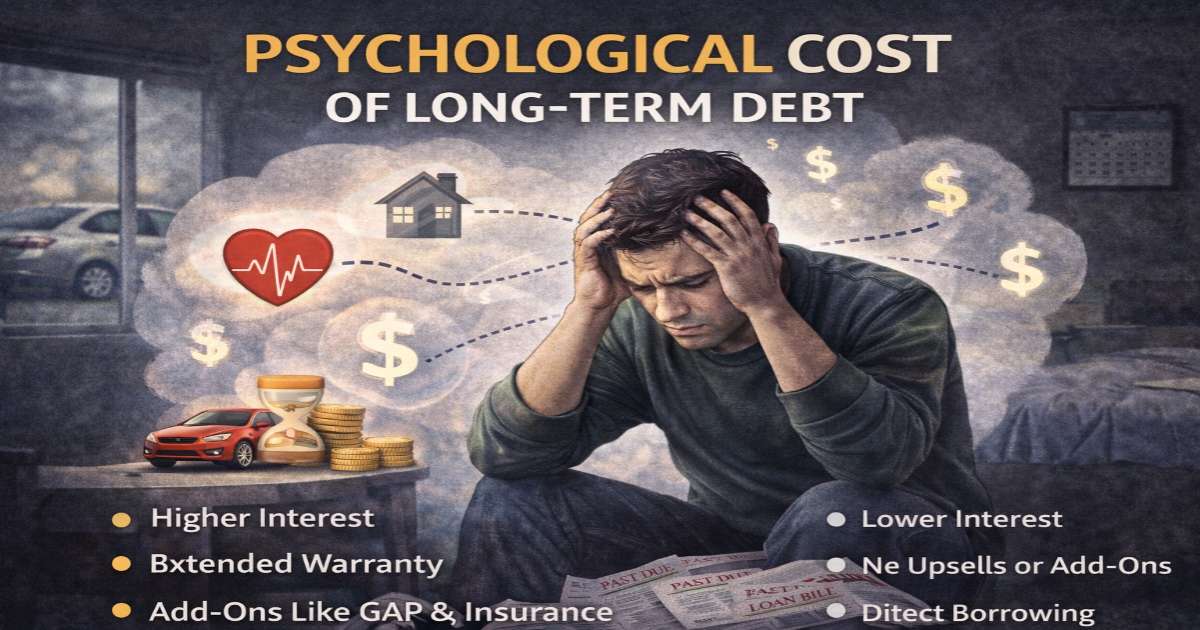

The Psychological Cost of Long-Term Debt

Beyond financial figures, long vehicle loans carry emotional and psychological costs that borrowers rarely anticipate. Being tied to a car loan for six or seven years can limit your financial flexibility and increase stress, especially if your income changes or unexpected expenses arise.

Long-term loan drawbacks often include:

- Reduced ability to save or invest

- Stress caused by long-term monthly obligations

- Limited options to upgrade or sell your vehicle

These hidden costs don’t appear on paper but can strongly impact your overall financial well-being.

Why Transparency Still Falls Short

Despite regulations, vehicle loan disclosures can be complex and overwhelming. Many borrowers sign agreements without fully understanding terms because the information is presented in dense legal language. Lenders may technically disclose costs while making them difficult to notice or interpret.

Common transparency issues include:

- Overly complex loan documents

- Key fees buried in fine print

- Verbal explanations that differ from written terms

Taking time to review documents carefully or even seeking independent advice can protect you from costly mistakes.

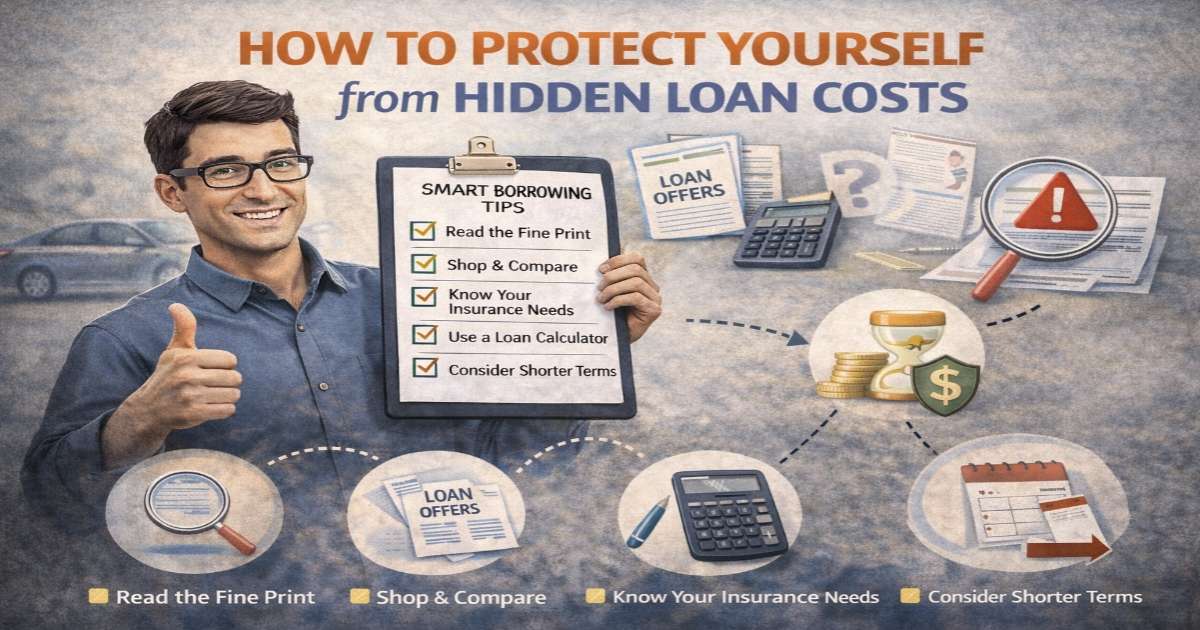

How to Protect Yourself from Hidden Loan Costs

Understanding the hidden costs of vehicle loans empowers you to make smarter financial decisions. Instead of focusing solely on monthly payments, evaluate the loan as a whole and ask detailed questions before signing.

Smart borrower strategies include:

- Comparing total loan cost, not just monthly payments

- Requesting a full breakdown of fees and add-ons

- Choosing the shortest loan term you can afford

- Getting pre-approved by multiple lenders

- Reading the loan agreement carefully, including fine print

Taking these steps can save you significant money and prevent unpleasant financial surprises down the road.

Smarter Ways to Reduce the True Cost of Vehicle Loans

Reducing the hidden costs of vehicle loans requires a proactive approach. Borrowers who prepare ahead of time and negotiate confidently are far more likely to secure fair terms and avoid unnecessary expenses.

Effective cost-saving strategies include:

- Making a larger down payment to reduce loan balance

- Choosing used vehicles with slower depreciation

- Avoiding unnecessary add-ons and upsells

- Negotiating interest rates and fees separately

- Reviewing loan documents before signing, not after

These steps help ensure your loan works for you instead of against you.

Final Verdict:

The hidden costs of vehicle loans don’t come from a single source, they build slowly through interest, fees, add-ons, and long loan terms. Lenders may not always highlight these expenses, but informed borrowers can spot them early and make better choices.

By focusing on total loan cost, understanding every clause and refusing unnecessary extras, you can take control of your financing decision and drive away with confidence rather than regret.

Frequently Asked Questions (FAQs)

Q.1: What are the most common hidden costs in vehicle loans?

The most common hidden costs in vehicle loans usually come from areas borrowers don’t examine closely at the time of signing. These include interest accumulated over long loan terms, bundled fees, and add-ons that are quietly financed into the loan amount. While none of these costs may seem excessive on their own, together they can significantly increase the total price of the vehicle.

Q.2: Why do lenders focus so much on monthly payments?

Lenders emphasize monthly payments because smaller numbers feel more manageable and appealing to borrowers. By extending the loan duration, lenders can reduce the monthly amount while increasing the total interest paid over time. This approach shifts attention away from the overall cost of borrowing.

Q.3: Are dealership vehicle loans more expensive than bank loans?

Dealership loans are not always more expensive, but they often carry hidden markups. Dealers may increase the interest rate offered by a bank or finance company and keep the difference as profit. This markup is rarely disclosed clearly to buyers.

Q.4: Do longer vehicle loan terms always cost more?

In most cases, yes. While longer loan terms reduce monthly payments, they almost always increase the total interest paid over the life of the loan. They also raise the risk of owing more than the car is worth for an extended period.

Q.5: Can paying off a vehicle loan early save money?

Paying off a vehicle loan early can save money on interest, but only if the loan does not include prepayment penalties. Some loans are structured so that interest is front-loaded, meaning early payoff savings are smaller than expected.